purchase a house in Canada – Many Canadians dream of buying a home. Since the beginning of the pandemic, the interest rates on housing loans were extremely low, but they started to grow again in 2022. It made many consumers close on homes or lock-in rates.

Do you know how to purchase a house in Canada? If you are just starting this journey, you may need this guide on what steps to take before you make this important decision.

Many Canadians who dream about becoming proud homeowners don’t know where to start. Whether you are planning to purchase a condo, a townhouse, or a fully-detached house, this process begins not when you arrange a house viewing with a realtor.

This process begins much earlier when you make this solution to make a big-ticket purchase. This decision should be precise and you need to understand that you are prepared for it.

This is a long-term commitment so taking the necessary steps and answering some questions may help you choose wisely.

Table of Contents

Decide If You Are Ready to purchase a house in Canada:

There are several questions you should ask yourself before you opt for this financial commitment.

- Are you financially prepared? When you live paycheck to paycheck you may only dream about getting online payday loans Winnipeg once in a while to cover your needs till the next salary day. If you don’t have enough savings, how can you manage mortgage payments?

- Do you have a down payment? Consumers who already have a down payment may find it easier to plan to get a home loan. They feel more prepared while those without this type of savings may struggle to try and find enough money for it. You may want to start budgeting to free up more money and allocate it toward savings for your future home or any business like custom rigid boxes startup.

- Do you have a steady income? It’s important to have a steady income source if you are about to purchase a home. Getting a mortgage means financial obligation so you need to have a consistent income to manage your monthly mortgage payments and avoid debt. Missed or late payments may lead to penalties and additional finance charges.

- Are you prepared to settle down? This is not a financial question but it’s also important. Are you sure you are ready to finally settle down? You may decide to review your personal and professional life to ensure you are where you would like to be so that such essential changes don’t make you feel stressed later.

HBO Max Black Friday is a powerful asset if you’re looking to up your holiday entertainment game:

What to Consider When Choosing a Home Loan.

You may find additional information on the mortgage options on the Government of Canada platform. It’s essential to understand how a mortgage can affect your financial stability and what home loan options are available out there.

When you decide to review your options and shop around for a home loan, make certain you opt for a product that fits your current needs. It should include your amortization, mortgage principal sum, and payment frequency.

The web platform offers free access to detailed information about every feature.

Get Pre-Approved for a Home Loan.

Of course, you need to be realistic about the type of house you can afford. If you get pre-approved for a home loan, you will be able to realize what size and type of home you may get. Crediting companies will conduct a credit inquiry when you apply.

They will review your credit rating so you should ensure it’s in good standing. Having an excellent or decent score boosts your chances of approval with the lowest rates.

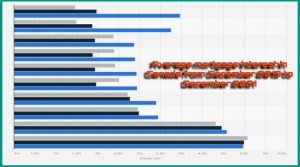

According to Statista, the interest rates on home loans in Canada lowered for almost all types of mortgages. Mortgages with insured fixed rates and less than one year term had the highest interest rate at 5.58 percent, while insured variable home loan interest rates were the lowest at 1.46 percent.

Average mortgage interest in Canada from December 2019 to December 2021, by mortgage term:

Besides, your current debt load, steady income, and down payment will be taken into consideration as you get pre-approved.

Try your best to minimize the existing debt load, repay the credit cards you have, and consolidate your debt. Having a sufficient down payment may also increase the odds of approval with the most affordable interest.

Get Your Finances in Order:

One of the most significant factors in getting a mortgage is having your finances in order. Can you manage your funds well? Are you good enough at budgeting?

You should have a steady source of income to have enough money set aside and make on-time payments. If you are unemployed, you won’t be able to make monthly mortgage payments, so lenders will most likely reject your application.

The next thing you should have is a down payment. It needs to be at least 5% of the total purchase price in Canada. Moreover, you will need to get mortgage loan insurance if the down payment for your house is less than 20%.

Some homes have different eligibility criteria to obtain a mortgage. For instance, houses with a purchase price of $500,000 or less may require just a 5% down payment, while homes with a higher purchase price will need a higher down payment.

Think About Government Assistance:

You may qualify for assistance from the government and incentives if you can’t afford to purchase a home on your own. Consumers may apply for the First-Time Home Buyer Incentive.

This program will give you 10% of the purchase price issued by the Canadian government. This incentive can only be used for first-time buyers.

Besides, you may choose the Home Buyers’ Plan, which is a widespread program in Canada. It allows the borrower to obtain up to $35,000 from their Registered Retirement Savings Plan (RRSP).

Couples and partners may benefit even more. If each of you takes out this sum, you will both have up to $70,000 together. This financial assistance should be repaid over time, the government usually gives borrowers about 15 years for debt payoff.

The Bottom Line:

Summing up, there are several steps you should take before you purchase a home in Canada. You need to answer some questions to ensure you are ready to become a homeowner and take this financial responsibility.

Getting your finances in order, having a budget, saving a down payment, and seeking assistance from the government may be beneficial for those who dream of purchasing a house.

Visit for more best articles